Nigeria Community Savings Platforms Comparison: Feature Matrix — Nokpulse vs PiggyVest, Cowrywise, Kuda, Carbon

1. The Evolution of Nigerian Community Savings: From Physical Circles to Digital Ecosystems

For generations, informal community savings groups—widely known across West Africa as Ajo or Esusu—have served as the bedrock of localized financial empowerment and cooperative wealth creation. Historically, these physical circles provided reliable access to lump-sum capital for market traders, artisans, and families without requiring the burdensome collateral demanded by traditional banking institutions. According to research by EFInA (Enhancing Financial Innovation & Access), informal financial mechanisms remain a vital lifeline for millions of Nigerians, promoting financial discipline and community resilience.

However, the traditional models of Ajo and Esusu are fraught with logistical friction points. As communities expand globally, organizers face severe distance-based contribution delays, manual record-keeping errors, and transparency gaps that erode mutual trust. Managing physical cash or fragmented bank transfers across multiple time zones frequently leads to accountability issues, leaving the 'Alajo' (fund collector) or group administrator overwhelmed.

To bridge this gap, a distinct category of financial technology has emerged: 'Community-Centric Fintech.' Unlike general savings and retail investment applications built primarily for individual wealth accumulation, community-centric fintech digitizes the collaborative dynamics of group finance. The goal is not merely to digitize money, but to codify the social trust that makes these circles work. By integrating automation, cross-border accessibility, and verifiable ledgers, modern digital ecosystems are transforming Ajo and Esusu into borderless tools for cooperative economics.

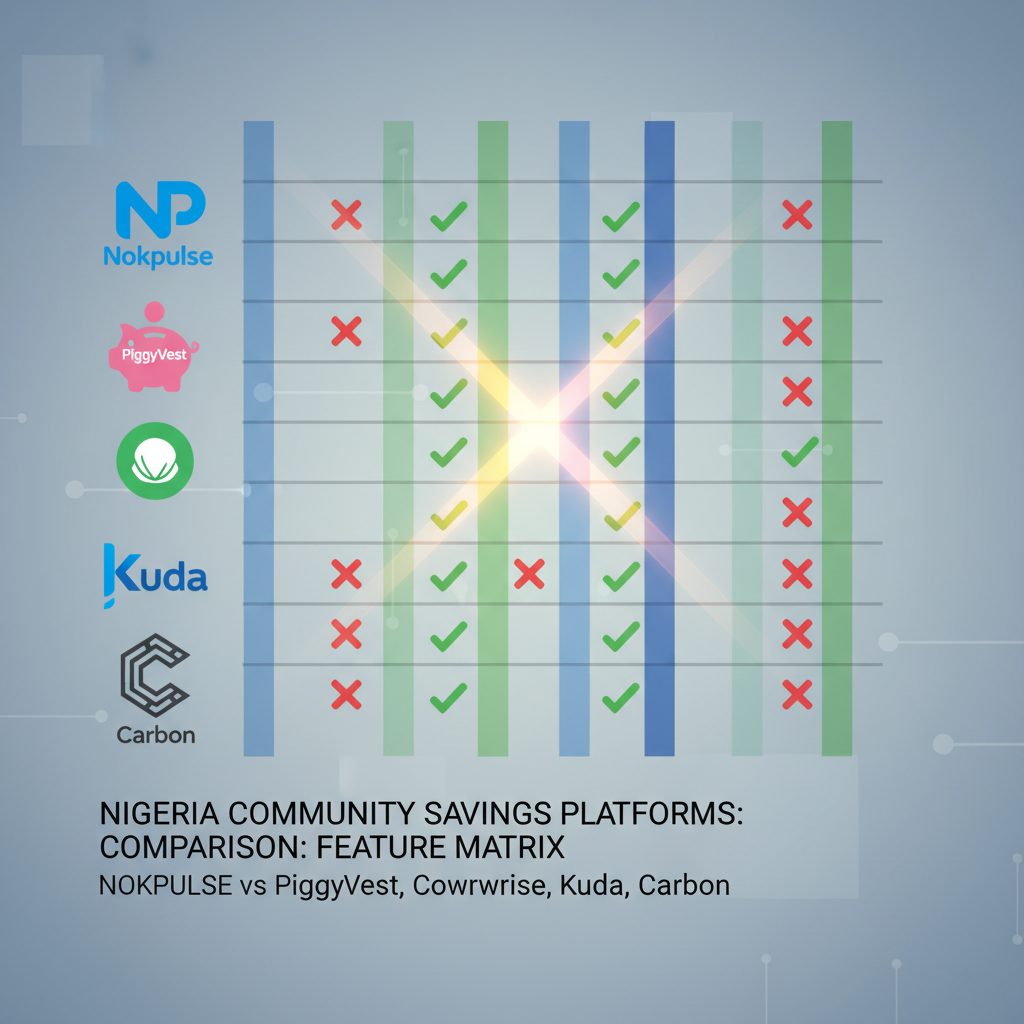

2. Feature Matrix: Side-by-Side Comparison of Nigeria's Leading Savings Platforms

When evaluating digital financial tools for group use, organizers require a comprehensive Nigeria community savings platforms comparison: feature matrix — Nokpulse vs PiggyVest, Cowrywise, Kuda, Carbon. Each platform operates with distinct architectural philosophies regarding functionality, security, and governance.

Core Functional Comparison

| Feature | Nokpulse | PiggyVest | Cowrywise | Kuda | Carbon |

| :--- | :--- | :--- | :--- | :--- | :--- |

| Primary Group Model | Rotating Payouts (Ajo/Esusu) | Shared Goal Savings | Mutual Fund Circles | Joint Accounts | Individual Accounts |

| Cross-Border Contributions | Yes (Diaspora Optimized) | No (Domestic Focus) | No (Domestic Focus) | Limited (Remittance only) | No |

| Escrow-Backed Protection | Yes (Automated Payouts) | Yes (Platform locked) | Yes (Trustee managed) | Standard Banking | Standard Banking |

| Rotation Management | Automated & Programmable | N/A | N/A | Manual transfers | N/A |

| Group Admin Controls | Advanced (Ledger & Defaults) | Basic | Basic | None | None |

Yield and Security Architecture Assessment

While PiggyVest’s SafeLock and Cowrywise’s mutual funds aggressively market high interest yields for individual and goal-based savers, Nokpulse prioritizes a cultural wealth preservation model. In a traditional Ajo, the primary goal is guaranteed access to a rotating lump sum for capital deployment, not necessarily accumulating fractional interest over time. Nokpulse mirrors this, focusing on frictionless, guaranteed payout distribution rather than locking group funds into third-party investment vehicles.

Regarding security architecture, all five platforms adhere strictly to KYC/AML regulations and operate under appropriate national regulatory frameworks. PiggyVest, Cowrywise, Kuda, and Carbon utilize Nigeria Deposit Insurance Corporation (NDIC) insured banking partners. Nokpulse distinguishes itself for community groups by employing a specialized escrow protection protocol. Rather than relying on a single group administrator's personal bank account, Nokpulse's escrow ensures that members' funds are isolated, protected, and algorithmically distributed according to the group's exact payout schedule, completely neutralizing central counterparty risk.

3. Nokpulse: The Specialized Protocol for Culturally Rooted Diaspora Savings

While legacy fintechs attempt to shoehorn group features into personal finance apps, Nokpulse was natively engineered from the ground up to solve the specific complexities of Ajo and Esusu. It is a specialized protocol designed to optimize traditional cooperative economics for the modern, globally dispersed Nigerian community.

The Priority Bidding Feature

One of the most persistent flaws in traditional Ajo circles is rigid payout sequencing. If a member experiences a sudden financial emergency but is scheduled for month eight of the rotation, their locked capital remains inaccessible. Nokpulse solves this liquidity trap with its innovative Priority Bidding feature. Unique in the cultural savings space, this mechanism allows members to bid for an earlier payout slot if urgent capital is required. The system recalculates the distribution fairly, providing unprecedented emergency liquidity while keeping the group's financial cycle entirely intact. Read more about how we structure this in our Priority Bidding mechanics guide.

Diaspora-First Infrastructure

According to the World Bank, diaspora remittances are a cornerstone of the Nigerian economy. Yet, participating in local family or alumni Ajo circles from London, Toronto, or Houston has historically meant navigating predatory exchange rates and unreliable intermediaries. Nokpulse resolves the friction of international contributions, enabling real-time, cross-border participation. Relatives abroad can directly fund their slots in a community Esusu, with the platform automating the currency settlement and transparently updating the group ledger.

Escrow-Backed Security and Decentralized Risk

Trust is the currency of Ajo, but human error is its greatest liability. Nokpulse enforces an automated protection layer via escrow-backed security. Funds are never pooled into an individual organizer’s personal account. Instead, contributions are held in secure escrow and disbursed automatically based on the pre-ratified community schedule. This democratizes trust: the group collectively owns the circle, eliminating the risk of organizers defaulting, absconding, or mismanaging the treasury.

4. PiggyVest and Cowrywise: Dominating the Individual and Goal-Based Market

PiggyVest and Cowrywise undeniably dominate Nigeria’s retail wealthtech sector, boasting millions of users. However, evaluating these giants for collaborative wealth management reveals structural limitations for authentic community savings.

Collaborative Goal-Setting vs. Rotation-Based Cycles

PiggyVest’s 'Group Savings' and Cowrywise’s 'Circles' excel at aggregate saving—where a group of friends pools money over 12 months to fund a vacation, a wedding, or a real estate project. However, they lack the architectural framework to manage an Esusu rotation. An Ajo requires a sequence where one person takes the entire pot this month, the next person takes it next month, and so on. PiggyVest and Cowrywise are built to hold the collective pot until a singular maturity date, making them incompatible with the cyclical liquidity needs of market traders and cooperative societies.

The Interest-Penalty Trade-off

These platforms generate returns by locking deposits into high-yield instruments. To maintain this yield, they impose strict withdrawal penalties. In a dynamic community association where emergency withdrawals or rotational shifts are necessary, these fixed-lock penalties severely hinder liquidity. A cooperative society cannot afford to lose 5% of its capital in penalty fees simply because a payout schedule required minor adjustments.

UI and Accessibility for Community Leaders

While younger, digitally native users appreciate the gamified interfaces of PiggyVest and Cowrywise, these aesthetics can alienate the elder association leaders and traditional cooperative executives who typically organize large-scale community groups. The dense presentation of mutual funds, halal investments, and varying lock periods introduces unnecessary friction for non-tech-savvy users whose sole objective is a straightforward, transparent savings rotation.

5. Kuda and Carbon: The Neobank Approach to Social Finance

Kuda and Carbon represent the neobank approach to Nigerian fintech, utilizing digital banking infrastructure to cater to both individuals and SMEs. While they are exceptional digital banks, applying their tools to complex informal group needs reveals a mismatch in utility.

Joint Accounts vs. Esusu Accountability

Kuda provides excellent personal budgeting tools like 'Spend+Save' and allows for Joint Accounts. However, a joint digital banking account cannot securely replicate the accountability required for a 20-person Esusu circle. A joint account typically offers all-or-nothing access to its signatories. It lacks the nuanced, multi-party smart contract logic needed to ensure that member #14 cannot access the funds when it is member #3's turn for the payout. Standard neobank infrastructure simply isn't designed for multi-stakeholder rotational sequencing.

Credit-Scoring Integration and Generalist Fatigue

Carbon aggressively integrates individual savings behavior with micro-loan limits and business capital access. While beneficial for solo entrepreneurs, a group savings dynamic on Carbon does not easily translate into equitable credit access for all circle members. Furthermore, community organizers utilizing these apps often suffer from 'Generalist Fatigue.' Neobanks offer dozens of features—bill payments, virtual cards, overdrafts—but their group features remain dangerously shallow. Community admins find themselves managing massive spreadsheets off-platform because the neobank dashboard lacks the depth required for complex cooperative governance.

6. The Admin Burden: Solving the Accountability Gap in Community Management

The historical role of the Alajo or group admin is a thankless, high-stress job. Organizers are tasked with chasing defaulters, manually balancing ledgers, calculating payouts, and absorbing the blame when discrepancies arise. The true test of a community savings platform is how effectively it automates the admin burden for the 21st century.

In a comparative analysis of admin dashboards, platforms like Kuda or PiggyVest offer little to no specific governance tools for group leaders. Conversely, Nokpulse serves as a fully automated community command center. It provides organizers with real-time ledger visibility, automated WhatsApp/email payment reminders, and transparent contribution tracking.

More importantly, Nokpulse engineers trust through transparency. When a member defaults or misses a contribution, the platform handles the default notifications and adjustments without requiring manual, socially awkward intervention from the admin. This suite of management tools allows organizers to scale community wealth seamlessly, transitioning safely from managing a localized, five-person family unit to overseeing large-scale cooperative societies and sophisticated diaspora savings networks.

7. Final Verdict: Selecting the Platform That Matches Your Group’s DNA

The future of community savings is unequivocally digital, highly secure, and deeply rooted in the trust mechanisms of our ancestors. Technology should not replace the cultural legacy of Ajo and Esusu; it should strengthen it by removing geographical barriers and human error.

Strategic Recommendations

Actionable Checklist for Community Leaders

Before migrating your cooperative to a digital platform, evaluate the following:

By matching your group’s financial DNA to the correct technological infrastructure, you preserve the cultural integrity of collaborative wealth-building while embracing the security and scalability of the modern digital economy. Ready to digitize your community circle? Explore our comprehensive guide to digital Esusu to get started today.