Nigeria Community Savings Platforms Comparison: Feature Matrix — Nokpulse vs PiggyVest, Cowrywise, Kuda, Carbon

Nigeria Community Savings Platforms Comparison: Feature Matrix — Nokpulse vs PiggyVest, Cowrywise, Kuda, Carbon

For generations, the cornerstone of wealth creation within African communities has been collective effort. When evaluating a Nigeria community savings platforms comparison: feature matrix — Nokpulse vs PiggyVest, Cowrywise, Kuda, Carbon, it becomes abundantly clear that while the personal finance sector has modernized rapidly, the community savings sector requires a specialized, culturally attuned approach. Today, the future of community savings is digital, secure, and deeply rooted in trust, paving the way for technology to strengthen our traditional wealth-building practices rather than replace them.

1. The Evolution of ROSCA in Nigeria: From Informal Circles to Digital Fintech — Understanding the $20 Billion Informal Savings Market

The historical transition from physical Ajo and Esusu collectors to digital Rotating Savings and Credit Associations (ROSCA) marks a pivotal moment in West African financial technology. For centuries, these community-driven financial circles have formed the backbone of the informal economy. According to data tracking financial inclusion by organizations like EFInA (Enhancing Financial Innovation & Access), the informal savings market in West Africa processes an estimated $20 billion annually. However, managing these funds manually carries profound risks.

Historically, Ajo relied entirely on verbal agreements and the personal integrity of a single collector or community leader. This trust-based system inevitably faced challenges, suffering from a default and mismanagement rate often exceeding 15% in informal circles. The shift toward smart-contract-inspired digital ledgers has begun to systematically eradicate these vulnerabilities.

Despite the clear need for modernizing this space, traditional banking applications have largely failed to accommodate the social and cultural nuances of group-mandated savings structures. Conventional banks view customers as isolated individuals rather than interconnected community members. They lack the specialized infrastructure to automate rotating payouts, enforce group accountability, or handle collective decision-making, leaving a massive gap in the market for platforms specifically designed to honor and elevate traditional community savings.

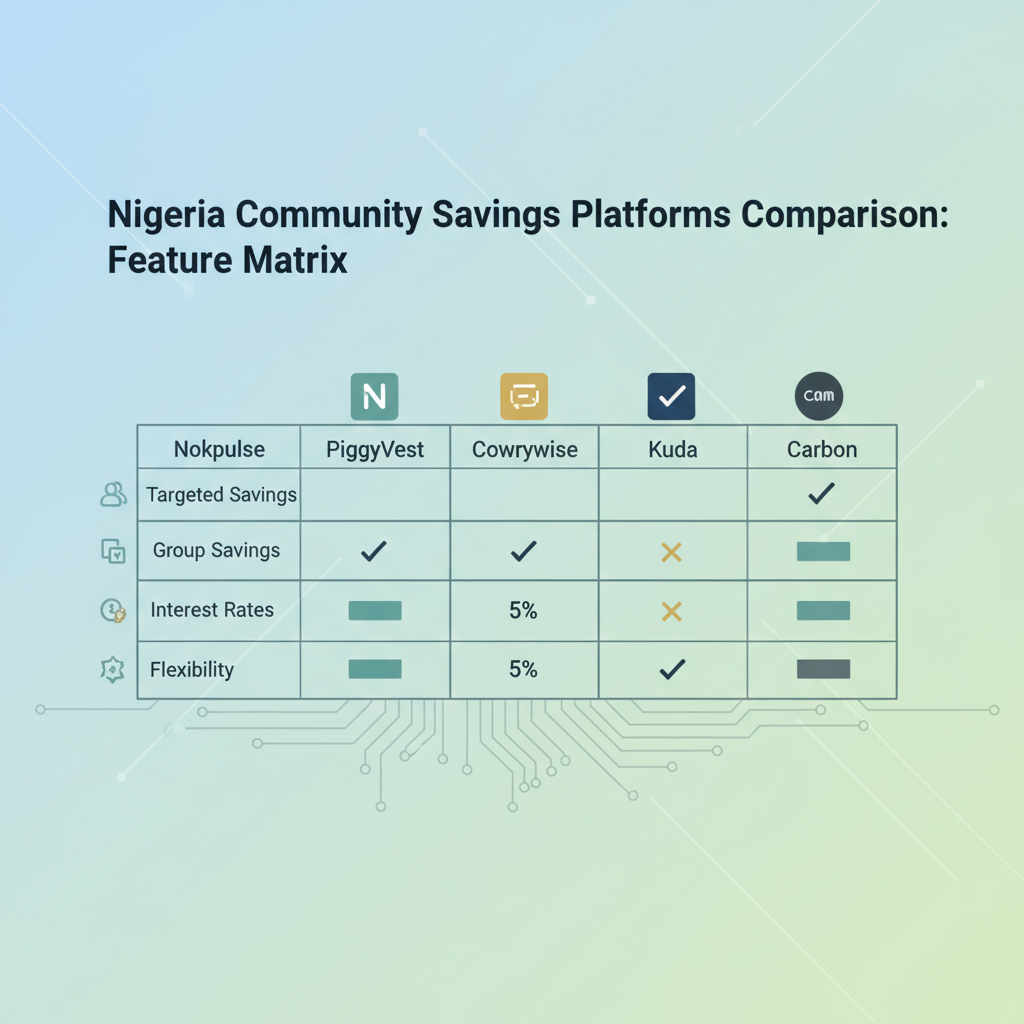

2. Comparative Overview: The Contenders in the Nigerian Savings Ecosystem — Positioning Individual Wealth Management vs. Community Wealth Creation

To understand the current Nigerian savings ecosystem, one must draw a clear line between individual wealth management and community wealth creation.

PiggyVest and Cowrywise have established themselves as indisputable leaders in the individual wealth management space. PiggyVest pioneered automated recurring savings, helping millions of young Nigerians build personal discipline through locked vaults and interest-bearing features. Cowrywise similarly excels by democratizing access to mutual funds and long-term individual investment portfolios. Both platforms thrive on personal financial independence.

On the banking front, Kuda and Carbon operate as premier neobanks. They provide robust "save-as-you-spend" features, instant micro-loans, and zero-fee personal transfers. However, their architecture is inherently individualistic. They offer peer-to-peer transfers but lack the dedicated cultural ROSCA infrastructure required to run a cooperative society or a family Esusu circle securely.

This is where Nokpulse introduces a paradigm shift. Nokpulse is a specialized, "Community-First" platform designed specifically to digitize the administrative and trust layer of traditional Ajo groups. While PiggyVest and Cowrywise ask, "How can an individual save more efficiently?" Nokpulse asks, "How can a community build wealth together seamlessly?" By focusing on group dynamics, Nokpulse provides a tailored ecosystem where religious groups, market associations, and diaspora families can safely pool capital, honoring cultural traditions while leveraging 21st-century technological safeguards.

3. Feature Matrix: A Data-Driven Technical Comparison — Analyzing Payout Models, Security, and Administrative Control

When we analyze the technical capabilities of these platforms, the divergence between individual-centric and community-centric architecture becomes stark.

Payout Models: PiggyVest utilizes a 'Target Savings' model, where users save toward a personal goal and withdraw upon completion. In contrast, Nokpulse employs an 'Automated Rotation' system designed for Esusu. In a Nokpulse circle, the platform automatically calculates contribution cycles and disperses the pooled funds to the designated recipient in the rotation queue, removing the need for manual distribution.

Security and Compliance: Traditional incumbents like Kuda and Carbon rely on standard Central Bank of Nigeria (CBN) licensing and basic data protection protocols to secure individual accounts. Nokpulse takes security a step further for group dynamics by utilizing a unique Escrow-backed security model. Because funds are pooled from multiple participants, Nokpulse holds these community funds in secure escrow. This guarantees that contributions are protected from internal group fraud and that the rotation cannot be broken by a single malicious actor, ensuring peace of mind for every contributor.

Administrative Control: Managing a group requires specific tools. While Kuda and Carbon facilitate easy peer-to-peer transfers, they do not offer group oversight. Nokpulse solves this through its comprehensive Admin Dashboard. Group organizers are granted unprecedented dashboard transparency, allowing them to track who has paid, who is defaulting, and the historical payout logs of the entire circle. This level of administrative control is nonexistent on personal wealth platforms.

4. The Diaspora Gap: Solving Cross-Border Community Contributions — Facilitating Global Ajo Circles from Lagos to London

African diaspora communities remain deeply connected to their roots, frequently participating in home-based projects, family associations, and investment circles. According to the World Bank's data on migration and remittances, diaspora remittances to Sub-Saharan Africa remain a critical economic driver. Yet, participating in a traditional Ajo from abroad introduces severe friction points.

Diaspora members constantly battle foreign exchange (FX) volatility, exorbitant remittance fees, and a fundamental lack of visibility. Sending funds across borders to a family member who manually logs contributions in a notebook creates a profound 'trust deficit'. Disputes over exchange rates at the time of contribution and uncertainty regarding payout schedules often deter diaspora participation.

PiggyVest and Cowrywise, while excellent locally, maintain a localized focus tailored primarily to domestic Naira accounts. Nokpulse’s architecture is fundamentally different. Built with global communities in mind, our platform enables seamless cross-border participation and multi-currency tracking. Through Nokpulse's Diaspora Circles framework, an immigrant in Toronto can contribute to the same Esusu as their sibling in Lagos. The real-time, transparent ledger ensures that diaspora members see exactly when their funds are received and when their payout is scheduled, effectively mitigating cross-border anxiety and removing the traditional barriers to global community wealth building.

5. Innovation Spotlight: The Priority Bidding and Escrow Mechanism — Modernizing the 'Who Goes First' Dilemma in Esusu

One of the most complex dilemmas in traditional Esusu is determining the payout order. Historically, the rotation is fixed, which creates rigidity. If a member in the sixth month of the rotation suffers a medical emergency in month two, traditional models offer no flexibility.

Nokpulse addresses this through a groundbreaking technical implementation: Priority Bidding. This exclusive feature allows members facing emergencies or sudden business opportunities to bid for an earlier payout within the app. By modernizing the "who goes first" dilemma, Nokpulse creates internal group liquidity without compromising the total savings pool. The member willing to pay a slight premium for early access can swap positions, creating a dynamic, responsive financial safety net.

Compare this to the 'Locked Savings' models of Cowrywise and Carbon. On those platforms, if you face an emergency and need to break your locked savings early, the platform penalizes you financially, effectively punishing you for needing your own money.

Furthermore, Nokpulse's escrow-backed mechanism transforms the risk profile of community savings. Funds are never held by a single group administrator. By holding the pooled capital in an independent escrow vault until the scheduled payout is triggered, Nokpulse ensures maximum security, removing the temptation and risk of theft that plagues informal collectors.

6. Governance and Accountability: Tools for Community Organizers — Empowering Cooperative Leaders with Professional Grade Management

Cooperative leaders, religious administrators, and market association executives carry the heavy burden of financial management, often relying on chaotic WhatsApp groups and easily corrupted Excel spreadsheets. Nokpulse professionalizes this role by providing a powerful 'Admin Tool Suite'.

This suite reduces the administrative workload by up to 80%. It features automated tracking of delinquent contributions and pushes automated SMS/email reminders to members before their payment is due. For transparency-heavy organizations like church groups or market trader associations, Nokpulse provides a public-facing group ledger. Every member can see the anonymized or identified contribution status of the group, enforcing social accountability.

By fully automating the payout logs and securely aligning with Nigeria Data Protection Regulation (NDPR) standards for privacy, Nokpulse entirely eliminates the disputes, record-keeping errors, and manual coordination fatigue that have historically limited the scalability of community savings associations.

7. Conclusion: Choosing the Right Platform for Your Savings Goals — Segment-Specific Recommendations for Nigerians at Home and Abroad

Choosing the optimal financial platform requires aligning software capabilities with your specific goals. If your primary objective is individual financial discipline and ring-fencing personal funds from daily expenses, PiggyVest remains a stellar choice. For individuals looking to passively invest in mutual funds and build long-term personal portfolios, Cowrywise is highly recommended. Neobanks like Kuda and Carbon are perfect for managing daily expenses and quick personal loans.

However, for cultural, community-driven wealth building, Nokpulse stands entirely in a league of its own. Nokpulse does not replace the centuries-old traditions of Ajo and Esusu; it actively preserves their integrity while fortifying them with 21st-century technical safeguards.

Digital ROSCAs represent the next frontier of financial inclusion for the underbanked and offer vital professionalization for the diaspora. By combining cultural authenticity with escrow-backed security, priority bidding, and transparent administration, Nokpulse proves that the future of community savings is not just about saving alone, but about building wealth together, securely, from anywhere in the world.